Dr. Arvind Kumar*

Our time accepting an uncomfortable truth: in the half-decade since COVID‑19, war has stopped being an exogenous shock to the global economy and instead become one of its operating logics, with energy corridors, arms supply chains and even multilateral institutions treated as levers in a larger geoeconomic game. The UNEP now speaks openly of a “triple planetary crisis”, warning that without “drastic action” and only collaboration “across our differences” can protect “the foundation of humanity’s existence”. Yet that collaboration is fraying just as conflict proliferates: the World Bank projects global growth slowing to 2.3 %, its weakest non‑recessionary performance since 2008, and warns that the 2020s risk becoming a “decade of squandered opportunities”, particularly for developing countries whose growth has already fallen below 4%.

The story began, of course, with the pandemic, which shattered supply chains and forced governments into massive fiscal expansions, leaving them with swollen debt, constrained policy space and electorates exhausted by austerity. As the health crisis ebbed, economic scarring and inflation remained, and the centre of the system entered a period of contradictory signals: headline growth surprised on the upside in 2024, but the IMF still sees US growth decelerating to around 2.2% in 2026 as high interest rates, a cooling labour market and policy uncertainty weigh on consumption and investment. That uncertainty is amplified by a visible retreat from multilateralism: withdrawal from dozens of international organisations and 32 UN‑linked agencies, moves that UN leaders describe as “deeply disappointing” and “contradicting the fundamental principles of multilateralism”. When the system’s anchor power simultaneously weaponizes tariffs and walks away from rule‑making tables, it is hardly surprising that the World Trade Policy Uncertainty Index has hit record highs and that small exporters in developing economies are forced to absorb the greatest shocks.

Into this fragile macroeconomic context crashed a chain of wars: Russia’s invasion of Ukraine, and now a direct Iran war that has turned much of West Asia into a live theatre, each conflict centred in one way or another on control over energy routes and strategic resources. Its latest Global Economic Prospects report underlines that the wider Middle East tensions have “heightened geopolitical risks” and that any escalation could send energy prices surging again, with cascading effects on global activity and inflation. These disruptions are not collateral damage at the margins of conflict; they are deliberate pressure points as one IMF analysis notes, about 15% of global maritime trade and over 10 per cent of seaborne oil transits these chokepoints.

Disruptions and delays

The latest Iran war has laid bare just how financialised and interconnected this war-economic order has become. Within days of Iranian missile and drone strikes on the UAE and retaliatory US‑Israeli operations, Dubai and Abu Dhabi’s stock indices fell by around 4–5%, prompting authorities to shut markets for two days in a bid to prevent panic. Oil, unsurprisingly, has spiked: Brent crude has jumped by more than 40% since the Iran war began, and analysts warn that strikes on refineries and shipping lanes could push prices higher still, fuelling inflation even in countries far removed from the battlefield. In a telling move, Washington has eased long‑standing sanctions on Venezuela’s oil sector, granting broad licences that allow US and allied firms to operate with PDVSA and route payments through US‑controlled accounts. Venezuela’s sudden rehabilitation is not a moral epiphany; it is a classic geo-economic adjustment in which an ostracised petro‑state is partially re‑integrated to cushion energy shocks created by another war.

Meanwhile, global military expenditure has soared to an unprecedented 2.7 trillion dollars, the steepest annual rise since the end of the Cold War, driven largely by the wars in Ukraine and broader tensions in Europe and the Middle East. SIPRI’s latest data show that US and Chinese defence budgets alone account for almost half of world military spending, with Russia’s outlays up to 149 billion dollars (around 7.1 % of its GDP) and Israel’s defence budget surging by roughly 65%. For the arms industry, war is not a tragedy but a demand curve: revenues for the world’s 100 largest weapons firms reached a record 679 billion dollars, rising 5.9 % in a single year, a boom that Action on Armed Violence bluntly describes as “an indictment of a global security system that treats war as a growth market”. At Europe’s biggest arms fair, manufacturers told Reuters with disarming candour that “war is good for business”, while French President Emmanuel Macron declared that his country had “entered a war economy” to meet surging demand. This is war-economics in its most literal form—conflict as a revenue model for a transnational military‑industrial‑financial complex.

It is about the strategic use of supply chains, currencies and corridors. A 2025 strategic review notes that states are increasingly “turning to economic tools as instruments of strategic influence”, whether in the US‑China trade war, sanctions on Russian energy, or the weaponisation of payment systems and critical technologies.

Yet when these geoeconomic projects touch the global South’s connectivity, they collide head‑on with war-economics. The India–Middle East–Europe Economic Corridor (IMEC), announced with fanfare at the 2023 G20 summit has been effectively stalled by Red Sea attacks. The Chabahar port and transit project, so central to India’s access to Afghanistan and Central Asia is repeatedly disrupted by US sanctions, and now faces renewed uncertainty as sanctions on Iran’s infrastructure tighten again. What was conceived as a shift “from geopolitics to geo‑economics” for landlocked states is once more hostage to great‑power confrontation. For developing economies, these blocked corridors translate into delayed investments, higher freight costs and missed opportunities to diversify away from chokepoints like the Suez Canal and the Strait of Hormuz costs their fiscally stretched governments can ill afford.

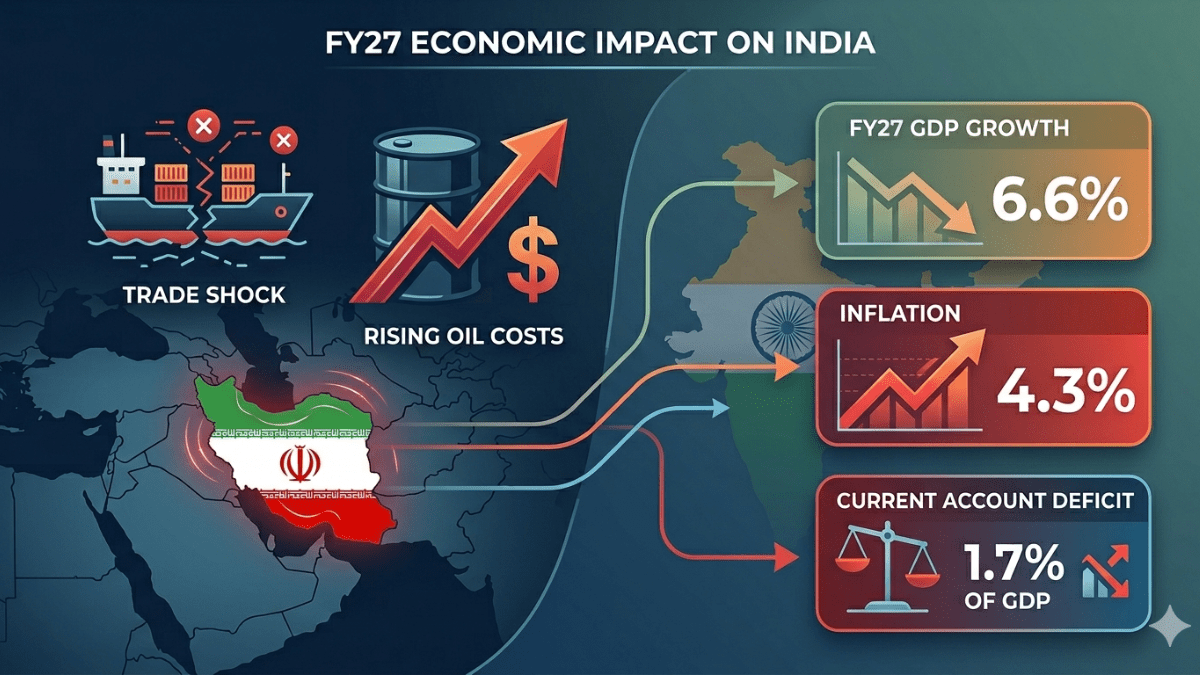

Nowhere is the asymmetric burden of war-economics clearer than in countries like India. Moody’s describes India as being in a macroeconomic “sweet spot”, projecting growth of around 6.6 % in 2025, underpinned by strong investment and infrastructure spending. Yet Indian policymakers know that this growth story rests on fragile foundations: external shocks to energy and food prices quickly spill over into domestic inflation, hitting poor households hardest. Measures are palliatives in a system where wars on another continent can still push up freight, fertiliser and LPG costs in Indian villages within weeks. Across the global South, the World Bank warns that “outside of Asia, the developing world is becoming a development‑free zone”, as growth decelerates, debt piles up and trade fragmentation erodes export prospects.

This raises a difficult question: Are these wars scripted in a smoke‑filled room to serve narrow interests? The pattern is hard to ignore. When arms‑industry revenues hit record; when energy sanctions, shipping disruptions and tariff wars simultaneously drive up prices and volatility for the poorest; then it is reasonable to say that war-economics has become a rational. Geopolitics and geoeconomics do indeed “run the world”, but the direction of travel is chosen by those who profit from instability while the brunt is borne by developing, weaker nations struggling with inflation, energy insecurity and the triple planetary crisis.

Way Forward

War-economics is not accidental it reflects a deliberate geoeconomic strategy in which powerful states and their industrial ecosystems derive advantage from managed instability, while developing nations absorb the costs through inflation, energy volatility, and disrupted connectivity. In response, developing economies must pursue pragmatic resilience: diversify energy sourcing through projects like Chabahar and expanded LNG capacity, strengthen currency stability via BRICS-led local trade mechanisms, and scale domestic defence manufacturing to reduce import dependence. Diplomatically, they should adopt calibrated neutrality while advocating reforms in IMF and World Bank governance for equitable representation. Over the long term, accelerating green energy transitions and deepening South–South trade integration can mitigate exposure to external shocks. In a fragmenting global order, coordinated multipolarity offers the most viable pathway to convert structural vulnerability into strategic autonomy.

*Editor, Focus Global Reporter